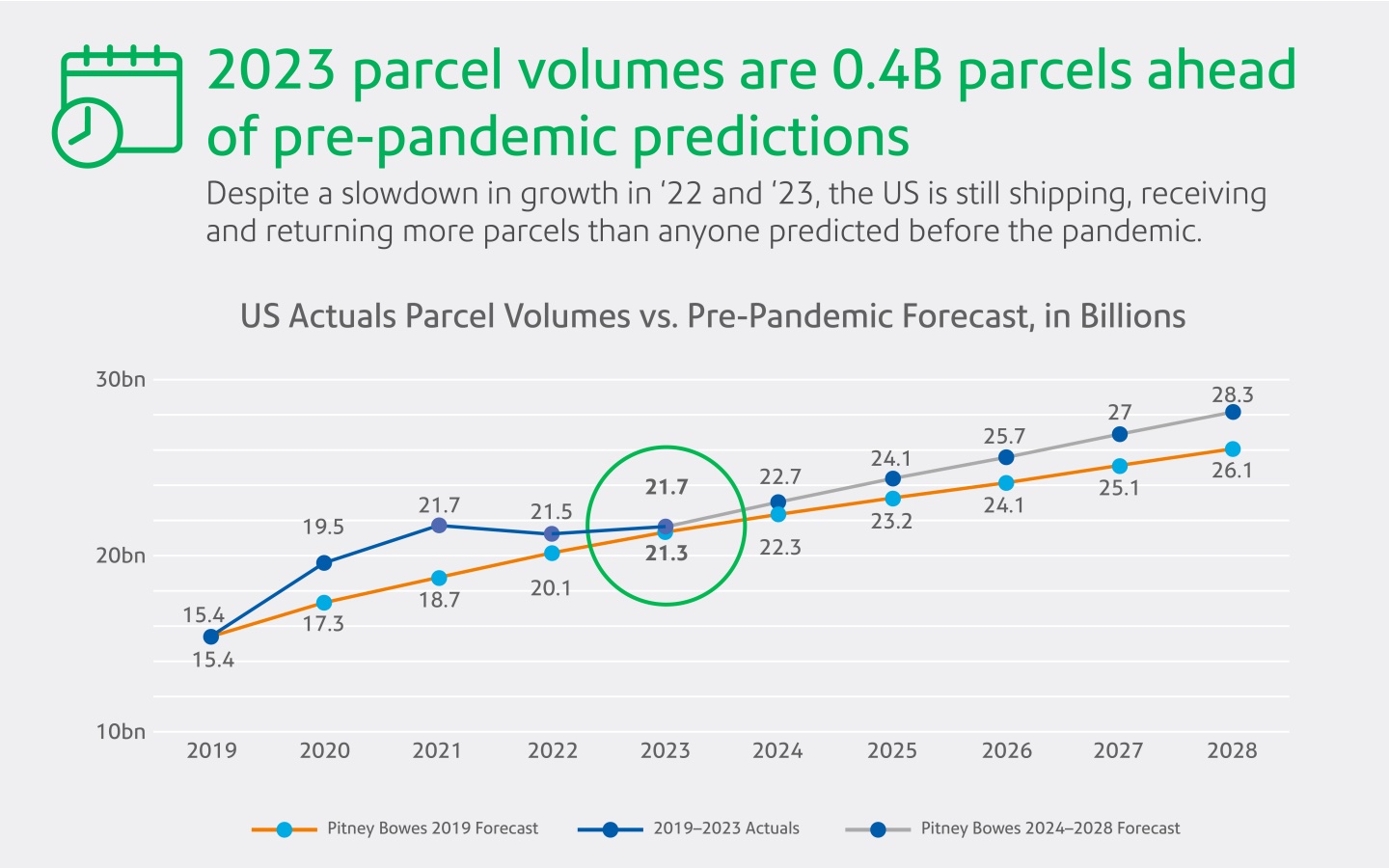

In 2023, US parcel revenue fell for the first time in seven years, from US$198.4bn in 2022 to US$197.9bn, despite total volume rising 0.5% from 21.5 billion in 2022 to 21.7 billion in 2023.

This is according to Pitney Bowes’ annual US Parcel Shipping Index, which reveals that of the four main carriers (USPS, Amazon Logistics, UPS and FedEx), only Amazon Logistics grew volumes year-over-year (YoY) – and by a hefty 15.7%. The company has also surpassed both FedEx and UPS in parcel volumes and is gaining on market leader USPS.

The report also shows that the ‘others’ category, which comprises smaller carriers, witnessed substantial growth in revenue and volume, with market share growing by 28.5% in 2023 to almost 3%, or 0.6 billion parcels.

“Despite the continued aftershocks of the Covid-19 pandemic, persistent inflation and pessimistic economic perceptions, consumer spending remains resilient, primarily via a growing demand for affordable goods from global marketplaces,” said Shemin Nurmohamed, EVP and president, sending technology solutions, Pitney Bowes. “The result is an influx of smaller, less-expensive, lightweight packages which drive up volumes at a lower rate of revenue-per-piece.”

According to Vijay Ramachandran, VP of go-to-market enablement and experience at Pitney Bowes, the legacy players are still adapting as the delivery landscape “shifts to favor natively direct-to-consumer parcel networks that are designed from the start to serve residential deliveries”. He added, “While parcel volume growth has shifted from double to single digits, consumers’ appetites for ‘real-time retail’, or affordable goods that are brought to market based on fast-moving trends, will continue to elevate parcel volumes well beyond the effects of the pandemic.”

Carrier volume and revenue

According to the report, USPS generated the highest parcel volume, at 6.6 billion parcels (down almost 1% YoY), followed by Amazon Logistics at 5.9 billion parcels (up 15.7%), UPS at 4.6 billion parcels (down 10.3%) and FedEx at 3.9 billion (down 6.1%) in 2023.

UPS generated the highest parcel revenue of the major carriers at US$68.9bn, down 6.4% YoY, followed by FedEx at US$63.2bn (down 3.1%), USPS at US$31.7bn (up 0.8%) and Amazon Logistics at US$28.6bn (up 19%). The ‘others’ category had the most significant revenue growth of 32.5% in one year, to US$5.6bn in 2023 from US$4.3bn in 2022.

UPS had the largest parcel revenue market share, with 35% of the market, a 2% decrease from 2022, followed by FedEx (32%), USPS (16%), Amazon Logistics (14%) and ‘others’ (2.8%).

Forecast

Pitney Bowes has forecast that US parcel volume will reach between 23 billion and 35 billion by 2029, with the most likely scenario that it will reach 29 billion with a 5% CAGR between 2024 and 2029.