From landlocked, ancient principalities to remote island states, there are 75 countries with populations of under one million – with posts for these smaller nations facing a number of unique challenges, including an acute imbalance between in and out flows of mail, write independent consultants, Elmar Toime and Adrian King.

Over 40% of all countries with a national postal operator have populations of under three million, and 20% of all nations have a land area of under 1,000km2 . Many of these nations are island states or otherwise enclosed within an envelope of larger countries. While they have a lot of features in common with the posts of larger countries, such as defined universal service obligations, their economic environment can be very different. Our experience, including serving on the boards of small postal companies or advising them, had us reflect on key issues that contrasted with the usual features of the larger postal companies.

In the strategies of the big operators, the dominant issues concern the domestic business. How should operations evolve to simultaneously manage population growth with more delivery addresses but with letter mail decline? How can the demand for 24/7 parcel delivery be reconciled with pressures to reduce universal obligations of five- or six-day delivery? In these economies the international aspects of the postal business typically have less impact. International revenue, through exports and imports, is less than domestic activity. Even with the growth of cross-border e-commerce volumes it has taken some time for pressure to have been applied to even out cost and pricing agreements between nations.

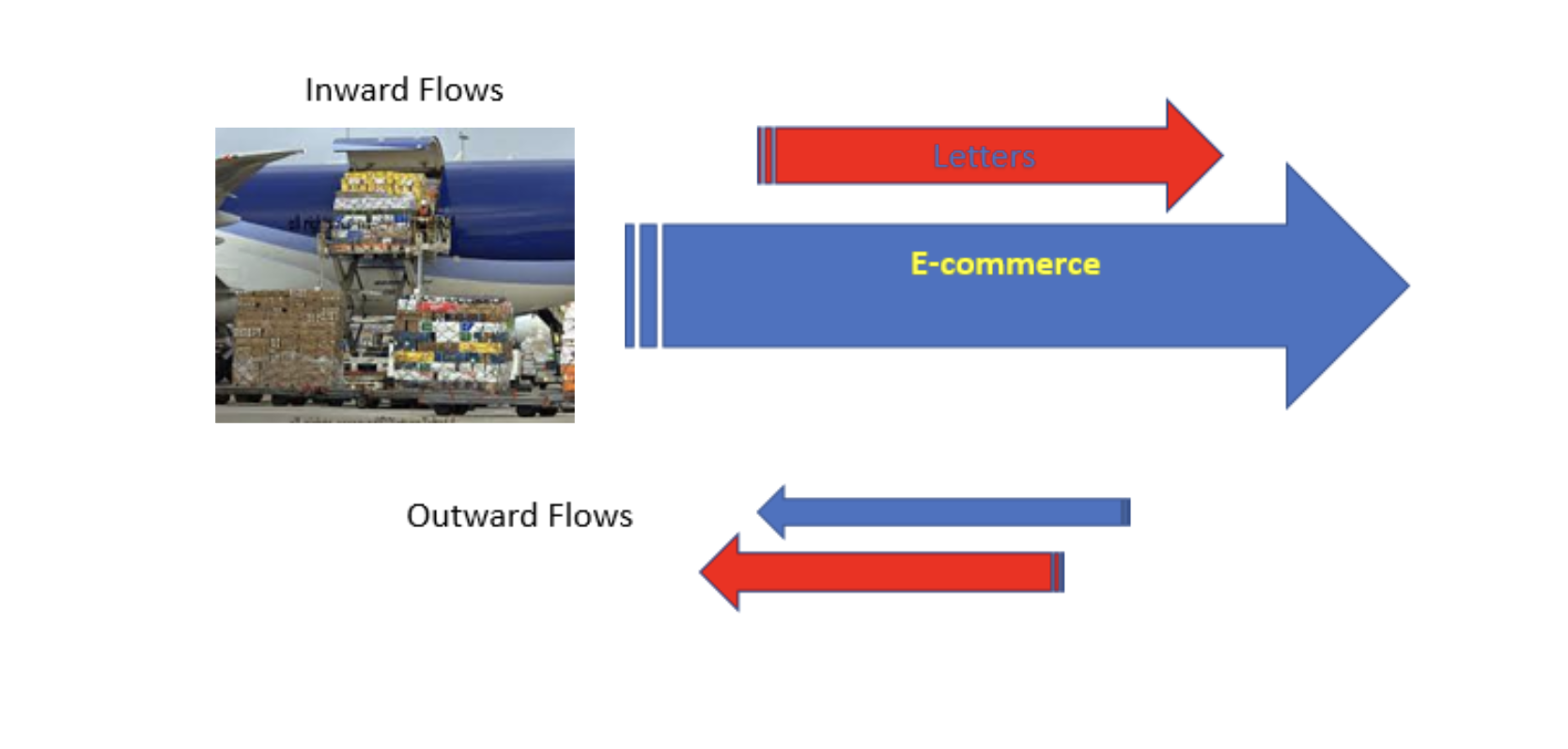

The small postal company at a superficial level may look the same. The volume trends and obligations are similar. One key difference is the dependence on international mail flows for the viability of the business. These posts will typically be net importers of mail and parcels, since the population is more dependent on goods and services from abroad. Because total revenue is relatively small, the decline in what was once a reliable income stream, letter mail, is challenging profitability. This exacerbates the overall strategy options in several ways. There is less cash to invest, whether in modernizing operations or trying to diversify. Depending on the overall national economy, the government may find it difficult to subsidize loss-making operations. Price rises are unlikely to generate adequate revenue growth and international rates for incoming mail are set externally.

Before exploring strategies, a word of caution. Strategy cannot ignore current competencies and reputation. A post, large or small, cannot expect to succeed in a diversification strategy if its present-day operations are inefficient or if the business does not have reputational gravitas.

In giving advice about strategic options, we would look at the different business segments and their opportunities.

Starting with the existing domestic core mails business, we know letter volumes will continue to decline and that e-commerce parcels will grow. These changes need to be modeled against trend scenarios to understand future pressure points in terms of pricing, revenue and productivity. What mix of actions should be considered, such as increasing prices, operational changes to better support parcel delivery, or even reductions in universal service obligations? A key issue in this market is the competitiveness of the postal parcel delivery service. If the post has low market share and poor quality, this must be the focus for immediate action.

Next, attention must turn to the international business. While posts often have a monopoly on inbound international mail, this is less relevant in the parcels market. Are exporting posts giving volumes to other domestic providers? Are non-postal operators and the international integrators controlling much of the parcel flow into the country and giving it to alternative last-mile agents? Depending on the situation there are a range of strategic choices:

- Create relationships with non-postal operators and become their deliverer of choice.

- Consider setting up sales operations in the most important import markets to win volumes at sources.

- Ensure that customs clearance processes use the full range of postal competitive advantage to improve the attractiveness of using the post.

With the changing complication of cross-border taxes, inspections and duties, e-commerce is moving toward bulk import. We are reaching a crossroads point here. Efficiency, speed, reduction in paperwork and import costs could in fact lead to a reduction in cross-border individual parcel volumes. If sellers gain traction in an international market it will be more efficient to ship products in by pallet load and have individual orders serviced by a warehouse agent. This is an immediate diversification opportunity for the postal company to operate import warehouse facilities. They could act as the customs broker, the warehousing agent, and the last-mile shipper and delivery agent.

With the changing complication of cross-border taxes, inspections and duties, e-commerce is moving toward bulk import. We are reaching a crossroads point here. Efficiency, speed, reduction in paperwork and import costs could in fact lead to a reduction in cross-border individual parcel volumes. If sellers gain traction in an international market it will be more efficient to ship products in by pallet load and have individual orders serviced by a warehouse agent. This is an immediate diversification opportunity for the postal company to operate import warehouse facilities. They could act as the customs broker, the warehousing agent, and the last-mile shipper and delivery agent.

Export activity of goods produced inside a small country is usually less than import business, unless the country has status as an import-export hub. Here, goods produced in one country and destined for another large market can transit through the hub, taking advantage of postal terminal dues processes. Where the small country is not operating as a hub, the post may be able to develop services to support domestic businesses. These may be for example artisanal goods produced on a small scale, but which may have the potential to sell overseas. The postal company can leverage its resources to provide a wider range of e-commerce services such as online marketplaces, international customer targeting and efficient distribution services.

From here a reasonable extension is to diversify into value-added distribution and logistics. What role could an efficient small postal company play in wider logistics chains? Are there opportunities to provide freight, fulfilment centers and other support activities, exploiting either postal status or other skills and investments?

While it appears to be a natural consequence that postal companies are increasingly turning into logistics businesses, there can also be opportunities to exploit existing investments in retail and digital services. Here they could develop roles in payment services or act as an agency for government. The post is uniquely placed to be the omnichannel manager of a government’s physical and digital engagement with citizens. Leadership for this may come from the government itself, or the post could exploit international digital identity developments to be a significant partner in a nation’s digital evolution. Once there is clarity on direction there is then a need to right size the post office network, using a combination of agencies, automated kiosks and online retail services through a portal. This creates a unique opportunity for the post to build customer relations with citizens and small businesses and further develop service offers.

As a final piece of advice, there needs to be government and policy clarity. The expectations for and regulation of the postal operator falls to government. The post is expected to provide societal and economic advantages to the nation. Too often postal policy is unclear and both government and management have expectations based on historic roles and perceptions. These may not help forward planning. The postal company needs to be brave and launch the debate on what sort of postal services will be wanted and that can be afforded in the longer term.

In conclusion, markets are changing. Posts need to change in alignment with market demands and requirements. Posts in small countries can still be an important infrastructure in a national economy, supporting flows of communication goods and payments as they have always done. They can remain an agency for growth and development in the economy. But this is not a given. Postal boards, management, and shareholders (whether government or private) need to think about what sort of postal business will be needed and sustainable in a decade’s time and what actions are required now to achieve that goal. There is one future which sees gradual decline of mail volumes, loss of relevance in parcel markets, and a declining role in payments and government services as they become digitized. This will inevitably lead to service diminution and financial instability. An alternative future is to review the themes defined in this review and develop a vision and action plan to define the small Post of the 21st century.

Elmar Toime has had a long career as a postal company CEO and supervisory board member. Based in London, he advises governments and postal companies on strategy and direction.

Elmar Toime has had a long career as a postal company CEO and supervisory board member. Based in London, he advises governments and postal companies on strategy and direction.

Adrian King has been a strategy consultant for over 30 years with a focus on the postal sector where he has led over 200 projects in many different countries. Based in London, his focus is on business development, strategic positioning, regulation, and operational reform.

Adrian King has been a strategy consultant for over 30 years with a focus on the postal sector where he has led over 200 projects in many different countries. Based in London, his focus is on business development, strategic positioning, regulation, and operational reform.